Pension Planning for Couples in Germany:

How Career Breaks, Children, and Income Gaps Affect Retirement

Table of Contents

Why Pension Planning for Couples in Germany Matters More Than Most People Realise

The German state pension system is built on a straightforward principle: you earn Entgeltpunkte (earnings points) for every year you work and contribute, and those points ultimately determine your monthly retirement income.

In theory, the system appears simple. In reality, however, Pension Planning for Couples in Germany is often far more complex than many people expect. While both partners may share the same household and financial goals, they rarely build pension entitlements at the same pace.

📌 Career breaks for childcare, part-time employment, periods of self-employment, and significant income differences between partners can create substantial pension gaps that continue long into retirement.

Over time, these differences can result in one partner receiving significantly less retirement income than the other, even after decades of working and contributing to the German pension system.

For this reason, effective pension planning Germany couples need should focus not only on individual pension rights but also on the long-term financial security of the household as a whole.

This guide explains how the system works, how pension gaps develop, and what practical strategies couples can use to protect their future retirement income.

How the German Pension System Works: Entgeltpunkte and the Rentenwert

Understanding the basics of the German pension system is essential for effective Pension Planning for Couples in Germany. While the system may seem complicated at first glance, it is fundamentally built around a simple concept: the more you contribute during your working life, the higher your future retirement income is likely to be.

Germany’s statutory pension system (gesetzliche Rentenversicherung) is administered by Deutsche Rentenversicherung and financed through mandatory pension contributions. Currently, the contribution rate is 18.6% of gross salary, shared equally between employees and employers, with each contributing 9.3%. This rate is defined under §158 SGB VI.

However, not all income is subject to pension contributions. For 2025, the Beitragsbemessungsgrenze (contribution ceiling) in the western federal states is EUR 96,600 per year (EUR 8,050 per month). Income earned above this threshold does not generate additional pension contributions or additional pension credits.

💡 The key building block of the German pension system is the Entgeltpunkt (EP), often referred to as an earnings point.

Each year, your Entgeltpunkte are calculated based on how your annual earnings compare to the national average salary (Durchschnittsentgelt). For 2025, the provisional national average income is EUR 45,358.

- If you earn exactly the national average, you receive 1.00 Entgeltpunkt for that year.

- If you earn more than the average, you receive more than 1.00 EP.

- If you earn less than the average, you receive proportionally fewer points.

Over the course of your career, these points accumulate and form the foundation of your future pension entitlement. This is one of the main reasons why pension planning Germany couples should pay close attention to income differences, part-time employment, and career interruptions, as even small variations can create meaningful pension gaps over time.

The final step in the calculation is the aktueller Rentenwert (current pension value), which converts accumulated Entgeltpunkte into monthly retirement income. As of 1 July 2024, the pension value is EUR 37.60 per Entgeltpunkt per month.

For example, a person who has accumulated 40 Entgeltpunkte throughout their working life would receive approximately EUR 1,504 per month from the statutory pension system (40 × EUR 37.60).

📌 Understanding how Entgeltpunkte are earned and converted into retirement income is the foundation of successful Pension Planning for Couples in Germany, as it allows both partners to identify potential pension gaps early and take action before retirement.

Pension Planning for Couples in Germany: Why Unequal Careers Create Unequal Retirements

One of the biggest challenges in Pension Planning for Couples in Germany is that retirement outcomes are rarely equal, even when both partners start their careers under similar circumstances.

A common pattern among German households is that one partner—statistically more often a woman—reduces working hours, takes extended parental leave, or temporarily steps away from the workforce to care for children. While these decisions may support family life in the short term, they often create a long-term pension gap that many couples underestimate until it is too late.

The reality is simple: lower earnings and fewer contribution years generally result in fewer Entgeltpunkte, which directly translates into a lower statutory pension during retirement.

⚠️ The most concerning aspect is that these pension gaps can continue for decades and are often difficult to fully close without proactive financial planning.

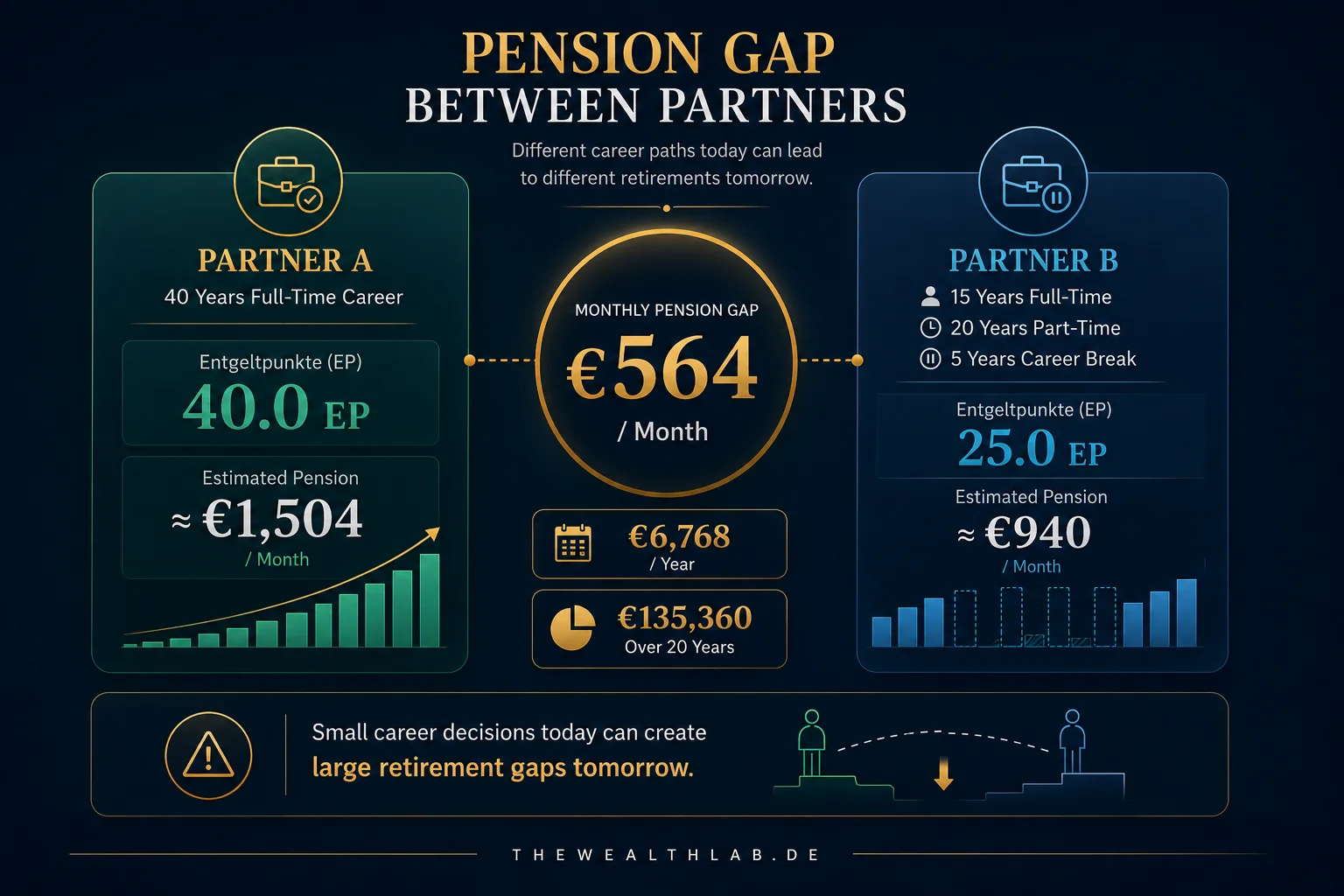

To illustrate the impact, consider two partners who both begin working at age 27 and retire at age 67, creating a 40-year contribution period.

Example Scenario

Partner A

- Earns the national average income throughout the entire 40-year career.

- Accumulates approximately 40.00 Entgeltpunkte (EP).

Partner B

- Earns the national average income for 15 years.

- Works part-time at approximately 50% of the average salary for 20 years.

- Leaves the workforce completely for 5 years.

As a result:

- Partner A: 40 years × 1.00 EP = 40.00 EP

→ Approx. EUR 1,504 per month (based on the 2024 Rentenwert) - Partner B: 15 years × 1.00 EP + 20 years × 0.50 EP + 5 years × 0 EP = 25.00 EP

→ Approx. EUR 940 per month

📉 Monthly Pension Gap: EUR 564

📉 Annual Pension Gap: EUR 6,768

📉 Lifetime Impact: Potentially tens of thousands of euros over the course of retirement

For many households, this difference can significantly affect financial security, lifestyle choices, and long-term independence during retirement.

It is important to note that this example does not include Kindererziehungszeiten (child-rearing pension credits), which can partially compensate parents for time spent raising children. However, even after accounting for these credits, the pension gap that many couples experience often remains substantial.

This is why Pension Planning for Couples in Germany should never focus solely on current household income. Couples should regularly evaluate future pension entitlements, identify potential retirement shortfalls early, and develop strategies to reduce the impact of career breaks, part-time employment, and unequal earnings before those gaps become permanent.

Entgeltpunkte by Salary Level: What Different Earnings Mean for Your Pension

The table below shows how annual salary translates into Entgeltpunkte and eventual pension income, using the 2025 Durchschnittsentgelt of EUR 45,358 and the Rentenwert West of EUR 37.60 as of 1 July 2024.

| Annual Gross Salary | Entgeltpunkte per Year | EP After 10 Years | EP After 20 Years | Monthly Pension from This Period (2024 rates) |

| EUR 20,000 | 0.44 EP | 4.4 EP | 8.8 EP | EUR 165.44 |

| EUR 30,000 | 0.66 EP | 6.6 EP | 13.2 EP | EUR 248.16 |

| EUR 45,358 (national avg) | 1.00 EP | 10.0 EP | 20.0 EP | EUR 376.00 |

| EUR 70,000 | 1.54 EP | 15.4 EP | 30.8 EP | EUR 579.08 |

EP = Entgeltpunkte. Monthly pension = EP x Rentenwert West EUR 37.60 (ab 1.7.2024). Average earnings EUR 45,358 (vorlaeufiges Durchschnittsentgelt 2025). Sources: Deutsche Rentenversicherung; Sozialversicherungs-Rechengroessen-Verordnung 2025; §70 SGB VI.

These figures illustrate why pension planning Germany couples who have one higher-earning and one lower-earning partner need to understand the compounding effect of income differences. A EUR 50,000 difference in annual earnings translates into more than EUR 1.10 per day in pension difference — for every year of that earning differential.

How Children Credit Your Pension: Kindererziehungszeiten Explained

One of the most important and most underused provisions in the German pension system is Kindererziehungszeiten (child-raising credit). German pension law grants automatic pension credits to the parent who primarily raised the child, regardless of whether they were working or not during that period.

The legal basis is §56 Abs. 1 SGB VI, available at gesetze-im-internet.de/sgb_6/__56.html. The duration of the credit depends on the year of birth:

| Child Born | Credit Period | Entgeltpunkte Credited | Monthly Pension Value (2024 rates) |

| After 31 December 1991 | 36 months (3 years) | Up to 3.0 EP | Up to EUR 112.80/month |

| Before 1 January 1992 | 24 months (2 years) | Up to 2.0 EP | Up to EUR 75.20/month |

Sources: §56 Abs. 1 SGB VI (gesetze-im-internet.de/sgb_6/__56.html). Rentenwert West EUR 37.60 ab 1.7.2024 (Deutsche Rentenversicherung). Figures are upper-limit estimates assuming no other simultaneous employment income during the credit period.

Each year of Kindererziehungszeit credits the parent with Entgeltpunkte at the level of the national average wage for that year — regardless of whether they were actually working. For a child born in 2010 (post-1991 rule), the parent receives up to 3 full Entgeltpunkte, worth up to EUR 112.80 per month in additional pension (at the 2024 Rentenwert West).

Important: only one parent can claim the Kindererziehungszeit credit for the same child in the same month. Couples must designate which parent receives the credit. By default, it goes to the parent who stayed at home. In most cases this maximises the lower-earning partner’s pension — but the designation can be changed retroactively. This election should be reviewed deliberately as part of pension planning.

Unsure how your career history affects your German pension entitlement?

We help couples and expats in Germany map their pension gaps, understand Kindererziehungszeiten credits, and build a plan to close the shortfall.

Career Breaks and Pension Gaps: What the Numbers Look Like

One of the most overlooked aspects of Pension Planning for Couples in Germany is the long-term impact of career interruptions. While taking time away from work may be necessary for childcare, health reasons, relocation, further education, or family responsibilities, these periods can leave lasting gaps in your pension record.

Unlike some European retirement systems, the German pension system does not provide a guaranteed pension simply because you have lived in the country for a certain number of years. Instead, your future retirement income is largely determined by the contributions you make and the periods that are officially credited to your pension record.

📌 In simple terms, fewer contribution years generally mean fewer Entgeltpunkte, which can result in a lower pension for the rest of your retirement.

The effect of a career break depends on the reason for the interruption and whether pension credits continue during that period.

Elternzeit (Parental Leave)

Parental leave is one of the most common causes of pension gaps, particularly among couples with children.

The first 12 to 14 months of Elternzeit are generally treated as pension-insured periods (Rentenversicherungspflicht-Zeiten). During this time, pension credits are calculated based on 100% of the national average salary, rather than your actual income.

However, once this period ends, unpaid parental leave does not automatically generate additional pension contributions unless it is covered by Kindererziehungszeiten, which can partially compensate for time spent raising children.

Mini-Job Employment

Mini-jobs can also affect long-term retirement income.

Under the current rules, mini-job employees are generally exempt from mandatory pension insurance contributions unless they actively choose to participate.

As a result, years spent exclusively in a mini-job may generate little or no Entgeltpunkte, potentially creating a pension gap later in life. In some cases, voluntary pension contributions can help reduce this effect.

Unemployment (ALG I)

Periods of receiving Arbeitslosengeld I (ALG I) do continue to generate pension credits, but usually at a lower level than full-time employment.

The pension contributions during unemployment are generally based on approximately 80% of previous earnings, meaning that Entgeltpunkte continue to accumulate, but at a slower pace.

⚠️ While unemployment does not completely stop pension growth, extended periods outside the workforce can still have a noticeable impact on future retirement income.

Self-Employment (Selbstständigkeit)

For many expats, freelancers, and entrepreneurs, self-employment creates one of the largest retirement planning risks.

Most self-employed individuals in Germany are not automatically required to contribute to the statutory pension system, although certain professions—such as teachers and some tradespeople—may be subject to mandatory participation.

For everyone else, years spent in self-employment without making voluntary pension contributions generate zero Entgeltpunkte.

Over time, these missing years can create a significant pension gap Germany couples often fail to recognise until much later in life.

💡 This is particularly important for expat entrepreneurs and freelancers, as a successful business does not automatically translate into future pension entitlement unless retirement planning is addressed separately.

Understanding how different career breaks affect pension accumulation is a crucial part of Pension Planning for Couples in Germany. The earlier these gaps are identified, the easier it becomes to develop a strategy that protects long-term retirement income and reduces the risk of unpleasant surprises later in life.

Voluntary Contributions: How to Buy Back Pension Points

For many couples, pension gaps develop gradually over time due to career breaks, self-employment, international moves, or periods spent outside the German pension system. The good news is that Pension Planning for Couples in Germany does not end once a gap appears.

In certain situations, Germany allows individuals to make voluntary contributions to the statutory pension system and improve their future retirement entitlement. These options can be particularly valuable for lower-earning partners, stay-at-home parents, self-employed individuals, and expats who have experienced interruptions in their contribution history.

📌 If identified early enough, pension gaps can often be reduced significantly through strategic planning and additional contributions.

Freiwillige Beiträge (§197 SGB VI) – Voluntary Contributions During Career Breaks

Individuals who are not currently subject to mandatory pension insurance can make voluntary contributions to the gesetzliche Rentenversicherung. This option is especially relevant for non-working spouses, certain self-employed professionals, and individuals who are temporarily outside the workforce.

The legal basis for voluntary contributions is §197 SGB VI.

By making voluntary payments, individuals can continue building pension entitlements even during periods when no mandatory contributions are being made. This can help reduce future pension gaps and improve long-term retirement income.

For 2025, the monthly contribution range is:

- Minimum contribution: EUR 100.07 per month

- Maximum contribution: EUR 1,503.80 per month

The exact amount can be chosen individually within this range, allowing contributors to balance affordability with their long-term retirement objectives.

💡 For many households, voluntary contributions can be an effective tool for strengthening the retirement position of the lower-earning partner and reducing inequality in future pension income.

Ausgleichszahlung (§187a SGB VI) – Compensating for Early Retirement Reductions

Another option available within the German pension system is the Ausgleichszahlung, a special compensation payment designed for individuals who plan to retire before the standard retirement age.

Under current rules, the standard retirement age is 67 for those born in 1964 or later. Retiring earlier generally results in a permanent reduction in pension benefits.

The reduction amounts to 0.3% per month of early retirement, which can lead to a total reduction of up to 14.4% for someone retiring four years before the standard retirement age.

⚠️ Because these reductions apply for life, the financial impact can be substantial over the course of retirement.

Under §187a SGB VI, individuals can make a lump-sum Ausgleichszahlung to partially or fully compensate for these future reductions. This effectively allows future pension benefits to be increased despite an earlier retirement date.

From the age of 50 onwards, Deutsche Rentenversicherung can provide a personalised calculation showing how much would need to be contributed to offset the planned reduction.

For couples considering early retirement, this can become an important part of retirement planning Germany strategies, particularly when one partner has significantly higher pension entitlements than the other.

📌 Voluntary contributions and compensation payments cannot solve every pension gap, but they can provide valuable flexibility for couples who want greater control over their future retirement income.

Versorgungsausgleich: How Germany Splits Pension Rights on Divorce

When discussing Pension Planning for Couples in Germany, many people focus on retirement savings, career breaks, and pension gaps. However, one important topic that is often overlooked is what happens to pension rights if a marriage ends.

Under German law, pension entitlements accumulated during a marriage are generally subject to a mandatory legal process known as Versorgungsausgleich (pension rights equalisation).

The legal basis for this process is §1 Versorgungsausgleichsgesetz (VersAusglG).

In simple terms, the pension rights earned by both spouses during the marriage are reviewed and, in most cases, divided equally between them. The purpose is to ensure that both partners share fairly in the pension entitlements accumulated throughout the relationship, regardless of differences in income or employment history.

📌 This rule applies to far more than just the statutory pension system.

The Versorgungsausgleich can affect a wide range of retirement arrangements, including:

- Deutsche Rentenversicherung entitlements

- Betriebliche Altersvorsorge (bAV) (company pensions)

- Riester-Rente contracts

- Beamtenversorgung (civil servant pensions)

- Other qualifying pension and retirement schemes

For many couples, this can have a significant impact on future retirement income projections.

For example, if one partner earned substantially more throughout the marriage and accumulated a higher number of Entgeltpunkte, a portion of those pension rights may be transferred to the lower-earning spouse as part of the equalisation process.

⚠️ As a result, the retirement income expected by each partner after divorce may differ considerably from the projections shown before the pension rights adjustment is completed.

This is particularly relevant for couples where one partner took career breaks, worked part-time, or stayed home to raise children. In these situations, the Versorgungsausgleich can play an important role in reducing long-term pension inequality between spouses.

From a retirement planning Germany perspective, understanding how pension rights would be treated in the event of a divorce is an essential part of comprehensive financial planning.

💡 Couples who are considering separation or divorce should strongly consider obtaining a professional Versorgungsausgleichsberechnung (pension equalisation calculation). This can provide a clearer picture of how pension rights may be divided and help both parties make informed financial decisions before finalising any agreements.

For many households, the impact of pension equalisation can be substantial, which is why it should never be overlooked when evaluating long-term retirement outcomes.

Riester-Rente: The State-Subsidised Top-Up for Couples

When it comes to Pension Planning for Couples in Germany, the Riester-Rente remains one of the most relevant government-supported retirement products, particularly for households where one partner earns significantly less than the other or temporarily leaves the workforce.

The Riester pension is a voluntary private retirement scheme that combines personal contributions with government support in the form of annual allowances (Zulagen) and, in some cases, additional tax advantages.

For many couples, it can serve as a useful supplement to the statutory pension system and help reduce future retirement income gaps.

2025 Riester Allowances (Zulagen)

Eligible participants may receive the following annual government subsidies:

- Grundzulage: EUR 175 per person per year

- To receive the full allowance, participants generally need to contribute 4% of their previous year’s gross income, up to a maximum eligible amount of EUR 2,100 including allowances.

- Kinderzulage:

- EUR 185 per year for each child born before 2008

- EUR 300 per year for each child born in 2008 or later

These allowances can significantly increase the overall value of a Riester contract over the long term, especially for families with children.

💡 For many households, the child allowance alone can make a meaningful contribution to long-term retirement savings.

One of the most attractive features of the Riester system for Pension Planning for Couples in Germany is the benefit available to non-working or lower-earning spouses.

If one partner holds an active Riester contract and meets the contribution requirements, the other spouse may also open a Riester contract and qualify for the full EUR 175 annual Grundzulage by contributing as little as EUR 60 per year.

This creates a cost-effective opportunity for the lower-earning partner to build additional retirement assets while benefiting from direct government support.

📌 In households where one spouse has taken career breaks, works part-time, or has significantly lower earnings, a Riester contract can be an effective way to strengthen individual retirement provision and reduce future pension gaps.

While the Riester-Rente is not suitable for every situation, it remains an important tool within retirement planning Germany strategies and can provide valuable support for couples seeking to build a more balanced and secure retirement income structure.

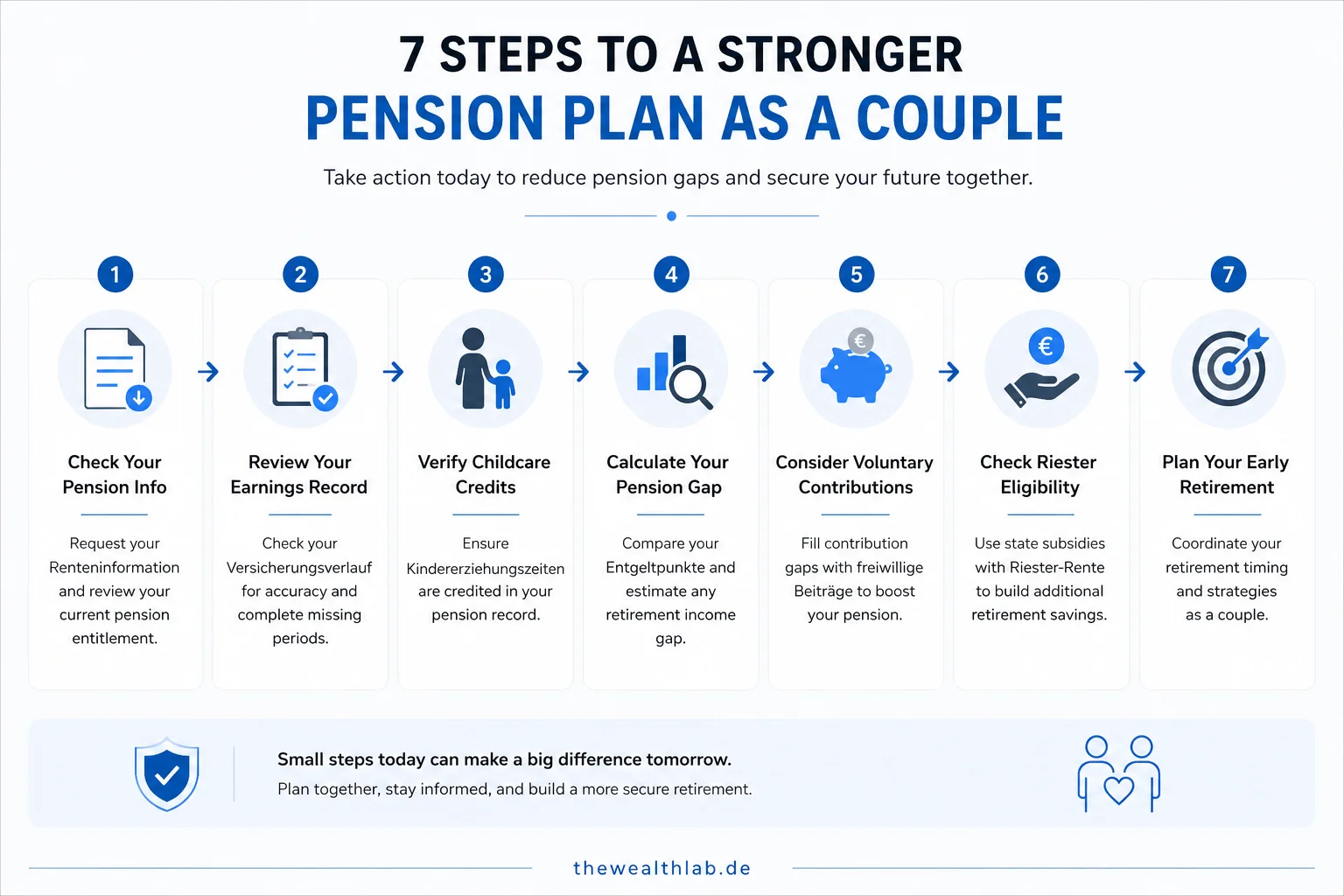

Pension Planning for Couples in Germany: A Joint Strategy Checklist

Understanding the rules of the German pension system is important, but taking action is what ultimately determines your future retirement income. For couples, regular reviews and proactive planning can help identify pension gaps early and create opportunities to strengthen long-term financial security.

📌 If you are serious about Pension Planning for Couples in Germany, consider working through the following checklist together.

1. Request and Review Your Renteninformation

Every partner should obtain and review their Renteninformation from Deutsche Rentenversicherung on a regular basis.

This document provides an overview of your current pension entitlement, estimated retirement income, and contribution history. Reviewing it annually can help you track your progress and identify potential issues before they become costly mistakes.

2. Check Your Versicherungsverlauf for Missing Periods

Your Versicherungsverlauf (contribution history) forms the foundation of your future pension entitlement.

Carefully review it for any missing or incorrect periods, particularly:

- Career breaks

- Elternzeit (parental leave)

- Unemployment periods

- Time spent abroad

- Self-employment periods

- Education and training periods that may qualify for pension credits

⚠️ Even small errors can affect your future retirement income if they remain uncorrected for many years.

3. Verify Your Kindererziehungszeiten Credits

If you have children, confirm that all eligible Kindererziehungszeiten have been correctly assigned to the intended parent.

Because these credits can have a meaningful impact on future pension benefits, it is important to ensure they are accurately recorded.

If you discover an error, you can request a correction through Deutsche Rentenversicherung.

4. Calculate Your Household Pension Gap

One of the most important steps in Pension Planning for Couples in Germany is comparing both partners’ projected retirement income.

Ask yourself:

- How many Entgeltpunkte has each partner accumulated?

- Is one partner significantly behind the other?

- How large is the projected retirement income gap?

💡 If a substantial difference exists, it may be worth exploring voluntary pension contributions under §197 SGB VI to strengthen the retirement position of the lower-earning partner.

5. Review Riester-Rente Eligibility

Many couples overlook the advantages available through the Riester-Rente system.

Non-working or lower-earning spouses may be able to open their own Riester contract and receive the full annual state allowance by contributing as little as EUR 60 per year, provided the other partner meets the eligibility requirements.

For some households, this can be one of the most cost-effective ways to build additional retirement provision.

6. Evaluate Self-Employment Risks

If either partner is self-employed, take time to assess how this affects your long-term retirement strategy.

Many self-employed individuals are not required to contribute to the statutory pension system, which means pension gaps can develop quickly if no alternative retirement planning is in place.

📌 Regularly reviewing whether voluntary pension contributions make sense can help reduce future shortfalls.

7. Explore Early Retirement Planning Options

If early retirement is part of your long-term goal, it is important to understand the financial consequences well in advance.

From age 50 onwards, you can request an Ausgleichszahlungsberechnung from Deutsche Rentenversicherung. This calculation shows how much would need to be contributed to offset the pension reductions associated with retiring before the standard retirement age.

By taking these steps early, couples can make informed decisions, reduce uncertainty, and build a more balanced retirement strategy together.

✅ The earlier pension gaps are identified, the more options you typically have to close them and improve your future retirement income.

FAQ: Pension Planning for Couples in Germany

Can both partners claim Kindererziehungszeiten for the same child?

No. Only one parent can receive the Kindererziehungszeit credit for a given child in a given month. However, the credit can be split between parents in different months during the credit period. The allocation should be reviewed carefully — in most cases directing the full credit to the lower-earning partner maximises overall household pension income.(Source: §56 SGB VI).

Does time spent abroad count towards the German pension?

Generally no. Years spent working abroad — unless in a country with which Germany has a bilateral social security agreement — do not generate German Entgeltpunkte. However, bilateral agreements exist with many countries (EU members, USA, Australia, Turkey, and others) that allow contribution periods to be combined for eligibility purposes. The actual pension calculation remains proportional to German contributions only. Check with Deutsche Rentenversicherung for your specific country of origin.

Can expats who leave Germany keep their German pension rights?

Yes. German pension rights (Entgeltpunkte and contribution years) are preserved even if you leave Germany. Non-EU nationals who have contributed for less than 5 years (60 months) may be eligible to claim a refund (Beitragserstattung) of their contributions upon leaving — though this forfeits all accrued pension rights. Those who have contributed for 5 or more years retain their rights and receive a German pension from retirement age, regardless of where they live. (Source: §§210-211 SGB VI).

What is the minimum pension in Germany?

Germany introduced the Grundrente (basic pension supplement) in January 2021, which automatically tops up the pension of anyone who has contributed for at least 33 years but received low pension credits due to low earnings. The supplement is calculated individually and does not require an application — Deutsche Rentenversicherung applies it automatically. (Source)

What is the standard retirement age in Germany?

The standard retirement age (Regelaltersgrenze) is currently 67 for all those born in 1964 or later. For those born between 1947 and 1963, the retirement age increases on a sliding scale from 65 to 67. (Source)

Ready to map your pension gap and build a plan as a couple?

Pension planning Germany couples need is rarely off-the-shelf. Whether you have career gaps, Kindererziehungszeiten questions, or are building a three-pillar strategy, we can help.

DISCLAIMER

The information in this article is for general educational purposes only and does not constitute financial, legal, or pension advice. The German pension system, including contribution rates, Entgeltpunkte calculations, Kindererziehungszeiten credits, and voluntary contribution rules, is subject to legislative change. All figures and examples are illustrative only and may not reflect your individual circumstances. The Wealth Lab is not a licensed financial, legal, or pension adviser. Before making any pension-related decisions, consult a qualified professional who can provide personalised guidance based on your specific situation.

About the Author

Sara Rahimi is a registered and independent financial consultant in Germany, specializing in financial planning for expats, professionals, entrepreneurs, and internationally mobile families.

She helps clients navigate the German financial system, including retirement planning, insurance strategies, investment planning, and long-term wealth building. Her work focuses on making complex financial topics easier to understand and helping individuals make informed decisions based on their personal circumstances and goals.

Through The Wealth Lab, Sara publishes educational content designed to help expats build financial confidence and better understand topics such as pensions, taxes, investing, and financial protection in Germany.

Leave a Comment

Have a question or experience to share? Drop a comment below.

Leave a Comment