Self-Employed Pension in Germany:

The Complete Retirement Guide for Expats

Table of Contents

If you’re self-employed in Germany, one question matters more than almost any other financial decision you’ll make:

Who is paying for your retirement?

For employees, retirement planning often happens quietly in the background. Every month, pension contributions are deducted automatically from their salary, employers contribute alongside them, and over time they accumulate statutory pension entitlements.

Self-employed professionals live in a completely different reality.

Whether you’re a freelancer, consultant, entrepreneur, contractor or business owner, your future retirement income largely depends on the financial decisions you make today. There is usually no employer contributing on your behalf, and in many cases you won’t automatically build significant retirement benefits through Germany’s statutory pension system.

That makes retirement planning one of the biggest financial responsibilities of being self-employed.

Unfortunately, it’s also one of the most neglected.

As a financial consultant working with expats across Germany, I’ve met entrepreneurs earning well into six figures who have no clear retirement strategy. Some assume that investing in ETFs alone will solve the problem. Others believe Germany will eventually provide enough pension income. Many postpone retirement planning because growing their business always feels more urgent.

The reality is that retirement planning becomes more expensive every year you delay it.

The earlier you begin, the more time your investments have to benefit from long-term compound growth. Waiting another ten years often means having to invest significantly more every month to work towards the same retirement goals.

That’s why this guide isn’t simply about pension products.

It’s about understanding how retirement actually works for self-employed professionals in Germany and how to build a strategy that supports both your lifestyle today and your financial independence tomorrow.

Whether you’ve just registered your freelance business or you’ve been running a successful company for years, this guide will help you understand:

- How the German pension system works

- 💼 Whether you must contribute to the State Pension

- 📈 The differences between Rürup, private pensions and ETF investing

- 💶 How taxes influence retirement planning

- 🛡️ How to protect your income before building wealth

- 🚀 How to create a long-term retirement strategy instead of buying random financial products

Rather than focusing on one “best” pension, we’ll look at how different retirement solutions can work together to build long-term financial security.

Let’s start with the foundation every self-employed expat should understand.

Understanding the German Pension System

One of the biggest mistakes expats make is assuming that retirement planning in Germany works the same way for everyone.

It doesn’t.

Germany’s retirement system is built around several different income sources rather than one universal pension.

Employees, civil servants, freelancers and business owners often follow very different retirement paths.

Understanding these differences is essential before choosing any retirement product.

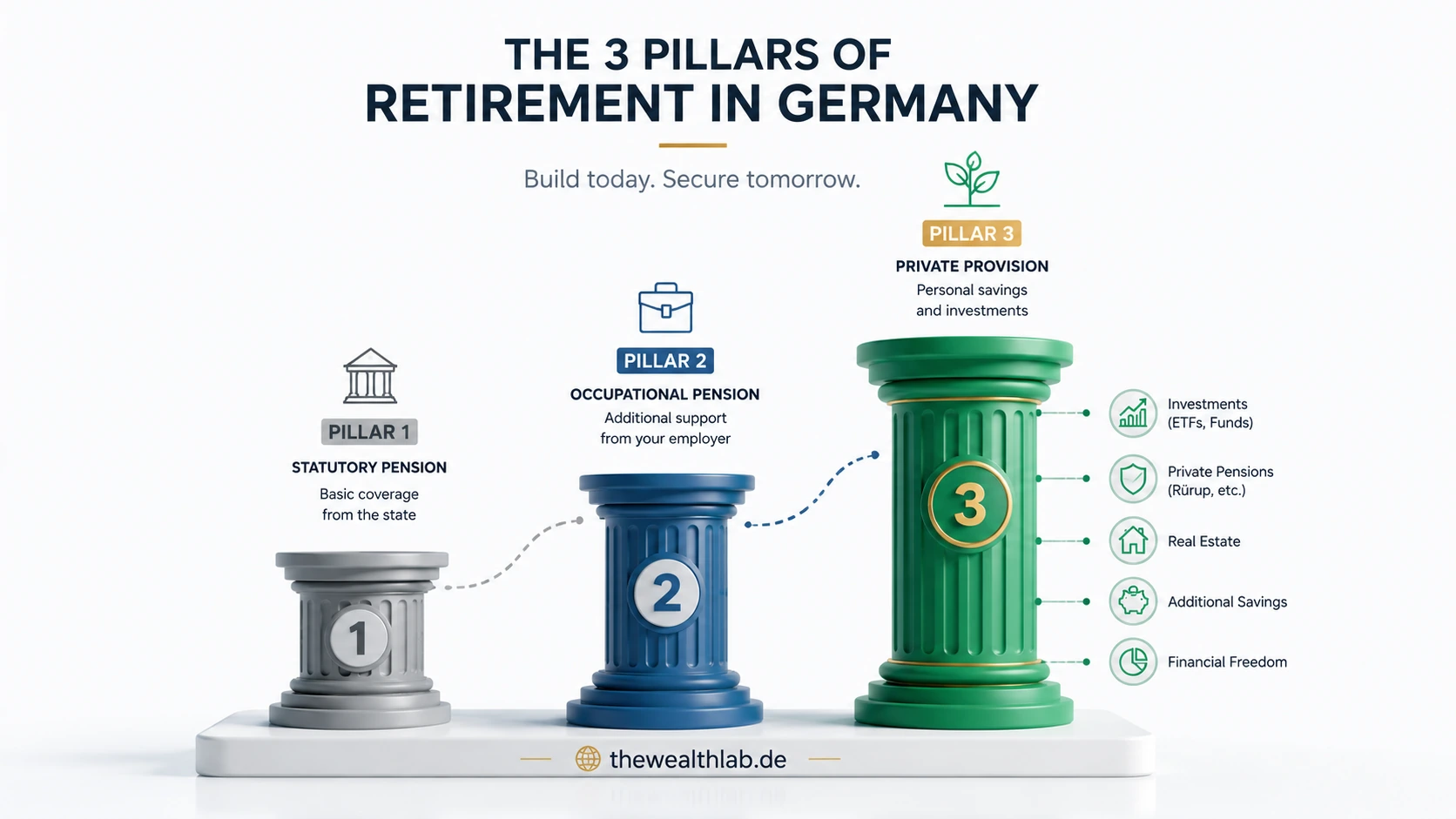

Germany’s Three-Pillar Pension System

Germany’s retirement system is commonly referred to as the Three-Pillar Pension System.

Instead of relying on one source of retirement income, the system combines different pillars that work together throughout retirement.

| Pension Pillar | Purpose | Importance for Self-Employed Professionals |

|---|---|---|

| 🏛️ Pillar 1 – Statutory Pension | Basic retirement income provided through the German public pension system. | May be mandatory for certain professions but is often limited or optional for many self-employed individuals. |

| 🏢 Pillar 2 – Occupational Pension | Employer-sponsored retirement benefits. | Usually not available unless you’re employed by your own company under specific circumstances. |

| 📈 Pillar 3 – Private Retirement Provision | Private pension contracts and long-term investments. | The most important retirement pillar for many self-employed professionals. |

For employees, these three pillars often work together automatically.

For self-employed individuals, however, the situation is different.

Many freelancers and entrepreneurs rely primarily on Pillar Three, making private retirement planning one of the most important financial decisions they’ll ever make.

Why Retirement Planning Is Different for the Self-Employed

Running your own business gives you freedom.

You choose your clients.

You decide your working hours.

Your income has the potential to grow without the limitations of a salary.

However, that freedom also comes with additional responsibility.

Unlike employees, self-employed professionals usually need to build their own retirement strategy from the ground up.

That means asking questions such as:

- Will I receive a German State Pension?

- Should I contribute voluntarily?

- Is a Rürup Pension suitable for me?

- Should I prioritise ETF investing instead?

- How much retirement income will I actually need?

- How can I reduce taxes while planning for retirement?

Without a clear strategy, it’s easy to spend years focusing exclusively on growing your business while neglecting your future financial security.

Are Self-Employed People Automatically Covered by the German State Pension?

This is one of the most common questions expats ask.

The short answer is:

Not necessarily.

Unlike employees, self-employed professionals are not all treated the same.

Whether you’re required to contribute to the German statutory pension system depends on factors such as:

- Your profession

- Your legal status

- The nature of your self-employment

- Specific provisions under German law

Certain professions may have compulsory pension insurance obligations, while many others organise their retirement independently.

For that reason, it’s important not to assume that registering a freelance business automatically means you’re building statutory pension entitlements.

Who May Be Required to Contribute?

Under German law, some self-employed professions may be subject to compulsory pension insurance.

Examples include certain independent:

- Teachers

- Midwives

- Childcare professionals

- Craftspeople in regulated occupations

- Artists and publicists covered through specific social insurance arrangements

The exact rules depend on your individual circumstances.

If you’re unsure whether compulsory pension insurance applies to your profession, you should verify your status before making retirement decisions.

What If You’re Not Required to Contribute?

Many expats initially see this as good news.

“No pension contributions means more money every month.”

In reality, it simply shifts the responsibility.

Instead of building retirement wealth automatically, you now need to build it intentionally.

Without regular contributions or long-term investing, retirement can become increasingly difficult to fund later in life.

For many successful freelancers, the biggest financial risk isn’t earning too little today.

It’s reaching retirement with substantial business income but insufficient retirement assets.

Can You Make Voluntary Contributions?

Yes.

Depending on your circumstances, voluntary contributions to the German statutory pension system may be possible.

Some self-employed professionals choose voluntary contributions because they want to:

- Increase future pension entitlements

- Build qualifying insurance periods

- Complement other retirement income sources

- Diversify their retirement strategy

Whether voluntary contributions are beneficial depends on your personal objectives, tax position, retirement timeline and overall financial situation.

There is no universal answer—which is exactly why retirement planning should always be personalised.

Is the German State Pension Enough?

This question doesn’t have a single answer.

Future pension income depends on many variables, including:

- Years of contributions

- Pension points accumulated

- Retirement age

- Lifetime earnings subject to contributions

- Future pension legislation

For many self-employed professionals, relying on a single retirement income source can increase financial risk.

A more resilient strategy often combines several retirement assets rather than depending entirely on one system.

Think of retirement planning as building a table.

A table supported by one leg is unstable.

A table supported by several strong legs is far more resilient.

The same principle applies to retirement income.

Instead of asking,

“Which pension product is the best?”

A better question is:

“How can I build multiple sources of retirement income that work together?”

That question will guide the rest of this article.

In the next section, we’ll explore the biggest retirement challenges facing self-employed expats and explain why simply earning a high income doesn’t automatically lead to long-term financial security.

The Biggest Retirement Challenges for Self-Employed Expats in Germany

Building a successful business is exciting.

Watching your income grow, finding new clients and expanding your business often become the main priorities during the first years of self-employment.

Retirement planning, on the other hand, usually feels like something that can wait.

Unfortunately, that’s exactly why many self-employed professionals fall behind.

Unlike employees, who build retirement benefits automatically through payroll deductions and employer contributions, freelancers and entrepreneurs need to create their own retirement system from scratch.

The challenge isn’t simply choosing the right pension product.

The real challenge is managing the unique financial risks that come with self-employment.

Let’s look at the most important ones.

No Employer Is Contributing to Your Retirement

One of the biggest financial advantages employees receive is something they rarely think about.

Their employer contributes towards their retirement.

If you’re self-employed, that contribution doesn’t exist.

Every euro that goes towards your future retirement comes directly from your own income.

This means retirement planning should be treated as a business expense—not something you only think about if money is left at the end of the month.

Successful entrepreneurs don’t invest only in their business.

They also invest in the person who will eventually stop working.

Your Income Isn’t Always Predictable

Many freelancers experience fluctuating income.

Some months are exceptional.

Others are much quieter.

Because of this, retirement planning often becomes inconsistent.

Many people tell themselves:

“I’ll start investing properly once business becomes more stable.”

The problem is that business often continues to evolve.

There is always another investment.

Another opportunity.

Another expense.

Without a structured retirement plan, years can pass without making meaningful progress.

A successful retirement strategy should be flexible enough to adapt to changing income while remaining consistent over the long term.

Inflation Quietly Reduces Your Future Purchasing Power

One of the biggest risks to retirement isn’t market volatility.

It’s inflation.

Money sitting in a current account slowly loses purchasing power over time.

While inflation rates change from year to year, the long-term effect remains the same:

The cost of living generally increases over time.

That means the amount of money needed to enjoy a comfortable retirement in twenty or thirty years will likely be much higher than it is today.

A retirement strategy should therefore focus not only on preserving wealth but also on helping it grow over the long term.

Living Longer Means Funding More Years of Retirement

People are living longer than ever before.

While this is good news, it also means retirement savings may need to last for several decades.

For many self-employed professionals, retirement is no longer a period of ten or fifteen years.

It may extend well beyond twenty or even thirty years.

This makes long-term planning increasingly important.

Rather than asking:

“How much money do I need when I retire?”

it’s often more useful to ask:

“How long might my retirement income need to support my lifestyle?”

Many Expats Won’t Retire in Germany

This is one of the biggest differences between expats and German nationals.

Many international professionals eventually relocate.

Some return to their home country.

Others retire somewhere with a lower cost of living.

Some divide their retirement between multiple countries.

These decisions can influence retirement planning in several ways, including taxation, pension rights and access to retirement income.

That’s why retirement planning for expats should always consider international mobility rather than assuming you’ll remain in Germany forever.

Paying Less Tax Should Never Be the Only Goal

Tax efficiency is important.

But retirement planning should never begin with the question:

“How can I pay less tax?”

Instead, start with:

“What kind of retirement do I want to build?”

Once that answer becomes clear, tax-efficient solutions can then be selected to support that goal.

The most effective retirement strategies usually balance:

- 📈 Long-term investment growth

- 💶 Tax efficiency

- 🛡️ Financial security

- 🌍 Flexibility for future life changes

- 💰 Sustainable retirement income

Tax savings are simply one part of the bigger picture.

The Cost of Waiting

Many people believe they have plenty of time.

“I’m only 30.”

“I’m only 35.”

“I’ll start next year.”

The challenge is that retirement planning rewards consistency more than urgency.

Starting earlier generally provides more time for investments to grow and may reduce the amount that needs to be invested later.

Waiting doesn’t just delay your retirement strategy.

It often makes achieving the same retirement goals significantly more difficult.

💡 Financial Consultant’s Perspective

One pattern appears again and again.

The clients who achieve the strongest long-term results aren’t necessarily those with the highest incomes.

They’re the ones who start early, stay consistent and regularly review their strategy as their lives and businesses evolve.

Retirement planning isn’t about predicting the future.

It’s about preparing for it.

Key Takeaways

Before choosing any retirement product, remember these principles:

✔️ Self-employment provides freedom—but also greater financial responsibility.

✔️ Retirement planning should be treated as part of running a successful business.

✔️ Inflation, longevity and income fluctuations all influence retirement planning.

✔️ Expats often need additional flexibility because they may not retire in Germany.

✔️ Building a retirement strategy starts with defining your goals—not choosing a financial product.

Now that we’ve explored the challenges, let’s compare the retirement solutions available in Germany—including the Rürup Pension, private pension plans, ETF investing and real estate—to understand how each can contribute to a well-diversified retirement strategy.

Comparing Retirement Options for Self-Employed Professionals in Germany

After understanding how the German pension system works and the unique retirement challenges faced by self-employed professionals, the next logical question is:

Which retirement solution is right for you?

The answer isn’t as simple as choosing one pension product.

Retirement planning is about building a financial strategy—not buying a single solution.

Every retirement option available in Germany has its own strengths, limitations and purpose. The right choice depends on your income, tax situation, retirement goals, investment horizon, risk tolerance and future plans.

For many self-employed expats, the most effective retirement strategy combines several solutions rather than relying on only one.

Let’s look at the most common retirement options available.

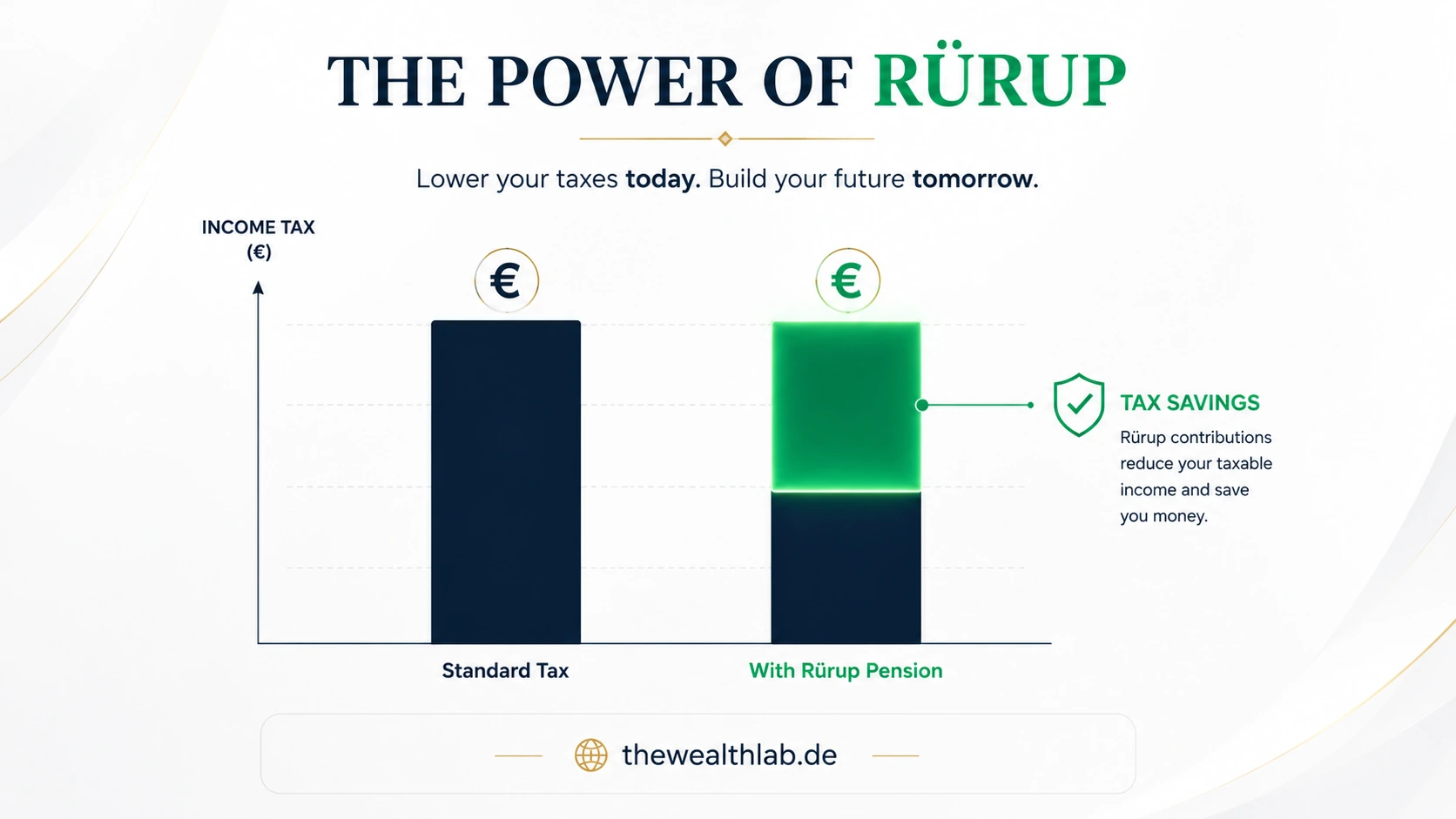

Rürup Pension (Basisrente)

The Rürup Pension, officially known as the Basisrente, was introduced to help people who are largely responsible for their own retirement planning—particularly self-employed professionals.

Today, it remains one of the most widely discussed retirement products for freelancers, consultants and business owners in Germany.

Unlike a traditional investment account, the Rürup Pension is specifically designed for retirement.

One of its defining characteristics is that contributions may offer valuable tax advantages under German tax law, subject to the applicable rules and annual limits.

For individuals with higher taxable incomes, this can make the Rürup Pension an attractive component of a long-term retirement strategy.

Potential Benefits

✅ Contributions may reduce taxable income within the applicable legal framework.

✅ It is specifically designed for long-term retirement planning.

✅ Assets are generally intended to remain dedicated to retirement rather than short-term spending.

✅ It can complement other retirement investments.

Important Considerations

Although the Rürup Pension offers attractive features, it isn’t automatically the right solution for everyone.

Before making a decision, it’s important to understand factors such as:

- Contribution flexibility

- Investment options

- Retirement payout structure

- Contract conditions

- Long-term accessibility of the invested capital

Choosing a retirement product should never be based solely on tax savings.

A pension should support your long-term financial goals—not simply reduce this year’s tax bill.

Private Pension Plans

Private pension plans represent another way to build retirement wealth independently of the German statutory pension system.

Unlike products specifically designed around statutory retirement rules, many private pension solutions offer greater flexibility regarding contributions, investment selection and retirement planning.

Depending on the provider and contract, these plans may allow policyholders to invest in professionally managed portfolios or investment funds while gradually building retirement capital.

For many expats, flexibility is one of the main reasons private pension plans become part of their overall retirement strategy.

Private Pension Plans May Be Suitable If You:

✔ You value flexibility.

✔ You want structured long-term retirement savings.

✔ You prefer regular monthly contributions.

✔ You want to complement other retirement assets rather than relying on one solution.

As with every financial product, understanding fees, investment strategy, contract terms and payout options is essential before making a long-term commitment.

Investing Through ETFs

During the past decade, Exchange Traded Funds (ETFs) have become one of the most popular long-term investment vehicles around the world.

Many self-employed professionals appreciate ETFs because they offer broad diversification, relatively low ongoing costs and exposure to global financial markets.

Unlike pension contracts, ETFs are investment vehicles rather than retirement products.

This distinction is important.

Investing and retirement planning are closely connected—but they are not the same thing.

A globally diversified ETF portfolio can help build long-term wealth, but retirement planning also involves questions such as:

- How much retirement income will you need?

- When do you plan to retire?

- How will withdrawals be managed?

- What happens if markets decline shortly before retirement?

- How should investment risk change over time?

For many investors, ETFs become one building block within a broader retirement strategy rather than the complete solution.

Why Many Investors Like ETFs

📈 Broad global diversification

💰 Low ongoing investment costs

🌍 Access to international markets

📊 Long-term growth potential

🔄 Flexible investing through monthly savings plans

Like every investment, ETFs also involve market risk, and their value can fluctuate over time.

For that reason, investment decisions should always reflect your individual objectives, time horizon and risk tolerance.

Real Estate as Part of a Retirement Strategy

Property has long been considered an important asset for long-term wealth building.

For some self-employed professionals, real estate becomes one component of retirement planning alongside pensions and investment portfolios.

Depending on your circumstances, property may contribute to retirement planning by:

🏠 Providing housing security in retirement

💶 Generating potential rental income

📈 Offering long-term capital appreciation

🛡 Helping diversify overall retirement assets

However, property ownership also comes with responsibilities and risks.

These may include:

- Financing commitments

- Maintenance costs

- Vacancy risk

- Property market fluctuations

- Transaction costs

Real estate should therefore be evaluated as part of an overall financial strategy rather than as a standalone retirement solution.

Comparing the Most Common Retirement Options

The table below provides a simplified comparison of some of the most common retirement solutions used by self-employed professionals in Germany.

| Retirement Option | Tax Efficiency | Flexibility | Growth Potential | Liquidity | Primary Purpose |

|---|---|---|---|---|---|

| Rürup Pension | ⭐⭐⭐⭐⭐ | ⭐⭐ | ⭐⭐⭐⭐ | Low | Long-term retirement income |

| Private Pension | ⭐⭐⭐ | ⭐⭐⭐⭐ | ⭐⭐⭐ | Medium | Flexible retirement planning |

| ETF Portfolio | ⭐⭐ | ⭐⭐⭐⭐⭐ | ⭐⭐⭐⭐⭐ | High | Long-term wealth accumulation |

| Real Estate | Depends on the situation | ⭐⭐ | ⭐⭐⭐⭐ | Low | Diversification and potential rental income |

Important: There is no universally “best” retirement option. The most suitable solution depends on your personal financial circumstances, retirement objectives and long-term plans.

Should You Choose Only One Retirement Solution?

In many cases, the answer is no.

Successful retirement planning is rarely built around a single financial product.

Instead, many self-employed professionals create a diversified retirement strategy by combining different assets that each fulfil a different purpose.

For example, one part of a retirement plan may focus on tax efficiency, another on long-term investment growth, and another on creating flexibility during retirement.

Diversification doesn’t eliminate investment risk, but it can help reduce dependence on any single source of retirement income.

💡 Financial Consultant’s Perspective

One of the biggest misconceptions I hear is:

“Which pension is the best?”

The better question is:

“Which combination of retirement solutions is most appropriate for my financial goals?”

Retirement planning isn’t about finding one perfect product.

It’s about building a strategy where every component has a clear purpose.

Key Takeaways

✔ There is no single retirement solution that fits every self-employed professional.

✔ Different retirement products serve different purposes.

✔ Tax benefits are important, but they should never be the only reason for choosing a pension.

✔ Diversification often plays an important role in building long-term financial resilience.

✔ Retirement planning should always reflect your personal goals rather than following someone else’s strategy.

In the next section, we’ll move beyond products and focus on something even more important:

How to build a complete retirement strategy that grows with your business and adapts as your life changes.

How to Build a Self-Employed Pension in Germany Strategy That Lasts

Understanding the available retirement products is only one part of successful retirement planning.

The real challenge is knowing how to combine them into a strategy that supports your lifestyle, adapts to your business and continues working for you over the long term.

A well-designed Self-Employed Pension in Germany strategy isn’t built overnight. It evolves as your income, family situation, tax position and retirement goals change.

Instead of asking:

“Which pension product should I buy?”

Ask yourself:

“How do I build a Self-Employed Pension in Germany strategy that still works twenty or thirty years from now?”

That shift in mindset changes everything.

Step 1: Define Your Retirement Goal

Every successful financial plan starts with a clear objective.

Before comparing products, estimate the lifestyle you want to maintain during retirement.

Consider questions such as:

- At what age would you like to retire?

- Do you plan to retire in Germany or abroad?

- Will you continue working part-time?

- How much monthly income would help support your desired lifestyle?

- Do you expect additional income from investments or property?

Your answers provide the foundation for building a realistic Self-Employed Pension in Germany strategy.

Without a destination, it’s impossible to choose the right route.

Step 2: Build Your Financial Foundation First

One of the most common mistakes is investing aggressively before building financial stability.

Before focusing on long-term retirement investments, make sure your financial foundation is strong.

A solid foundation often includes:

✅ An emergency fund covering approximately three to six months of essential living expenses.

✅ A realistic monthly budget.

✅ Sustainable cash flow within your business.

✅ High-interest debt under control.

Retirement planning becomes much easier when short-term financial emergencies don’t force you to interrupt your long-term investment strategy.

Step 3: Protect Your Ability to Earn an Income

Before building wealth, protect the income that makes wealth building possible.

For many self-employed professionals, the greatest financial asset isn’t their investment portfolio.

It’s their ability to generate income.

If illness or disability prevents you from working for an extended period, your retirement contributions may stop at exactly the time you need them most.

For this reason, income protection is often considered an important part of a comprehensive Self-Employed Pension in Germany strategy.

Protecting your income helps protect your future retirement as well.

Step 4: Diversify Your Retirement Assets

Many investors spend years searching for the perfect retirement product.

In reality, long-term financial security often comes from diversification rather than perfection.

Instead of relying entirely on one retirement solution, consider how different assets can complement one another.

A diversified Self-Employed Pension in Germany strategy may include:

| Retirement Asset | Purpose |

|---|---|

| 🏛️ Statutory Pension (where applicable) | Basic retirement income |

| 📈 ETF Portfolio | Long-term capital growth |

| 🛡️ Private Pension | Structured retirement savings |

| 💶 Rürup Pension | Tax-efficient retirement planning for eligible individuals |

| 🏠 Real Estate | Diversification and potential rental income |

| 💰 Emergency Savings | Financial flexibility |

Each component has a different role.

Rather than competing with one another, they work together to create a more resilient retirement strategy.

Step 5: Automate Your Retirement Contributions

One of the simplest ways to improve consistency is automation.

Successful retirement planning often relies less on timing the market and more on investing regularly.

Automating contributions helps remove emotion from financial decisions and encourages long-term discipline.

Whether you contribute monthly, quarterly or annually, consistency often matters more than trying to find the “perfect” time to invest.

For many people, a disciplined contribution schedule becomes one of the strongest drivers of long-term success.

Step 6: Review Your Strategy Every Year

Your Self-Employed Pension in Germany shouldn’t remain unchanged for decades.

Life changes.

Businesses grow.

Income fluctuates.

Tax legislation evolves.

Family responsibilities increase.

Your retirement strategy should evolve alongside these changes.

An annual review provides an opportunity to assess:

- Whether your retirement goals have changed.

- Whether your contribution level remains appropriate.

- Whether your investment allocation still matches your risk tolerance.

- Whether your retirement income target is still realistic.

Small adjustments made regularly are often more effective than major corrections later in life.

A Practical Roadmap for Self-Employed Professionals

Building a Self-Employed Pension in Germany doesn’t need to happen all at once.

Breaking the process into manageable phases can make retirement planning much easier.

| Phase | Primary Focus |

|---|---|

| Foundation | Build an emergency fund, stabilise cash flow and define retirement goals. |

| Growth | Begin regular retirement contributions and build diversified investments. |

| Optimisation | Improve tax efficiency, review pension solutions and increase contributions as income grows. |

| Maintenance | Review your strategy annually and adjust it as your personal and financial circumstances change. |

Think of retirement planning as an ongoing process rather than a one-time decision.

Common Signs Your Retirement Strategy May Need Reviewing

You may benefit from reviewing your current Self-Employed Pension in Germany strategy if any of the following apply:

⚠️ Your income has increased significantly.

⚠️ You’ve recently become self-employed.

⚠️ You’re relying on a single retirement product.

⚠️ You haven’t reviewed your retirement plan in several years.

⚠️ You’re unsure how much retirement income you’ll actually need.

⚠️ You plan to move abroad in the future.

These situations don’t necessarily mean your current strategy is wrong—but they are good reasons to reassess whether it still aligns with your long-term goals.

💡 Financial Consultant’s Insight

The strongest retirement strategies aren’t usually the most complicated.

They’re the ones that are reviewed consistently, adjusted when necessary and followed with discipline over many years.

Long-term financial success rarely comes from making one perfect decision.

It comes from making many good decisions consistently.

Key Takeaways

✔ A successful Self-Employed Pension in Germany strategy begins with clear retirement goals.

✔ Protecting your income is just as important as building retirement wealth.

✔ Diversification can help create multiple sources of retirement income.

✔ Regular investing often matters more than trying to time the market.

✔ Reviewing your retirement strategy each year helps keep it aligned with your changing circumstances.

In the next section, we’ll explore how tax planning, choosing the right financial adviser and avoiding common retirement mistakes can strengthen your Self-Employed Pension in Germany even further.

Tax Planning and Professional Guidance for Your Self-Employed Pension in Germany

Choosing the right retirement products is only one part of building a successful Self-Employed Pension in Germany strategy.

The other part—and often the one that’s overlooked—is making sure your retirement plan remains efficient as your income, business and personal circumstances evolve.

A retirement strategy that works well today may not be the most suitable strategy five or ten years from now.

That’s why long-term retirement planning isn’t a one-time decision.

It’s an ongoing process.

Tax Efficiency Should Support Your Retirement Goals

One of the biggest mistakes self-employed professionals make is choosing retirement products purely because they offer tax advantages.

While tax efficiency can be an important benefit, it should never become the primary objective.

Instead, think of tax planning as a tool that supports your overall Self-Employed Pension in Germany strategy.

The right question isn’t:

“Which product saves the most tax?”

It’s:

“Which strategy helps me build sustainable retirement wealth while making efficient use of the available tax rules?”

A balanced retirement strategy considers both today’s tax position and tomorrow’s retirement income.

Your Retirement Strategy Should Grow With Your Business

One of the advantages of being self-employed is that your income has the potential to increase over time.

As your business grows, your retirement planning should evolve as well.

For example, regular reviews may help you decide whether it’s appropriate to:

- Increase your monthly retirement contributions.

- Diversify your retirement assets.

- Reassess your investment allocation.

- Improve the tax efficiency of your retirement strategy.

- Adjust your retirement income goals.

A Self-Employed Pension in Germany should never remain static while your financial life continues to change.

Choosing the Right Financial Adviser

Many expats feel overwhelmed by the number of retirement products available in Germany.

That’s understandable.

Retirement planning isn’t simply about comparing products.

It’s about understanding how different financial solutions work together.

When looking for professional support, consider asking questions such as:

✔ Does the advice take my personal goals into account?

✔ Is my retirement strategy designed for my individual circumstances?

✔ Are the advantages and limitations of each option explained clearly?

✔ Do I understand the long-term costs, flexibility and potential risks?

The quality of advice is often just as important as the financial products themselves.

A Retirement Review Checklist

Whether you’re just starting your retirement journey or reviewing an existing plan, the following checklist can help you identify areas that may deserve attention.

| ✔ Retirement Planning Checklist | Status |

|---|---|

| I know whether I’m required to contribute to the German State Pension. | ☐ |

| I have defined my retirement goals. | ☐ |

| My Self-Employed Pension in Germany strategy is diversified. | ☐ |

| I contribute towards retirement on a regular basis. | ☐ |

| My retirement investments match my risk tolerance. | ☐ |

| I review my retirement strategy at least once a year. | ☐ |

| My retirement planning reflects my long-term goals and future plans. | ☐ |

Completing this checklist won’t create a retirement strategy by itself.

However, it can help you identify areas that may require further attention.

Common Retirement Planning Mistakes

Building a successful Self-Employed Pension in Germany isn’t only about making good decisions.

It’s also about avoiding common mistakes.

❌ Waiting Until Later

Many people believe they’ll start retirement planning once their business becomes more successful.

Unfortunately, time is one of the most valuable resources in long-term investing.

Starting earlier generally provides more opportunities for compound growth than trying to catch up later.

❌ Focusing Only on Tax Savings

Tax deductions can be valuable, but they shouldn’t determine your entire retirement strategy.

Your retirement plan should support your future lifestyle—not just reduce this year’s tax bill.

❌ Depending on One Retirement Product

No single investment or pension solution is likely to meet every retirement objective.

Diversification helps reduce dependence on one source of retirement income and can create greater financial resilience over time.

❌ Never Reviewing Your Retirement Plan

Many people set up a retirement product and never look at it again.

However, businesses evolve.

Income changes.

Family circumstances change.

Markets change.

Your Self-Employed Pension in Germany should evolve as well.

Regular reviews help ensure that your retirement strategy continues to reflect your current situation and long-term goals.

❌ Thinking Retirement Planning Can Wait

Perhaps the most expensive mistake is believing there will always be more time.

Retirement planning rewards consistency.

Even relatively small contributions made regularly over many years may have a meaningful impact compared with waiting several years before getting started.

💬 Financial Consultant’s Perspective

The most successful retirement plans I’ve seen have one thing in common.

They aren’t built around chasing the latest investment trend or finding the “perfect” pension product.

They’re built around a clear strategy, reviewed regularly and adjusted as life changes.

That’s what turns retirement planning into long-term financial confidence.

Final Thoughts

Building a successful Self-Employed Pension in Germany isn’t about predicting markets or finding a single perfect financial product.

It’s about creating a strategy that reflects your goals, adapts as your business grows and supports the lifestyle you want in the future.

Every self-employed professional has a different journey.

Your profession, income, tax position, investment experience and long-term plans are unique.

That’s why retirement planning should never rely on assumptions or generic advice.

The earlier you begin building your Self-Employed Pension in Germany, the more flexibility you’ll typically have to adapt your strategy over time.

The goal isn’t simply to retire.

The goal is to retire with confidence, knowing you’ve built a financial plan that’s designed around your life—not someone else’s.

FAQ: Self-Employed Pension in Germany

Is a Self-Employed Pension in Germany mandatory for all freelancers?

While there is no general mandate for most self-employed professionals, specific groups (e.g., artists, teachers, or midwives) are legally required to contribute to the state system. For the vast majority, establishing a personal Self Employed Pension in Germany is a voluntary but essential step to ensure long-term financial stability.

How does a Rürup Pension Germany differ from a Private Pension Germany?

The Rürup Pension Germany is specifically designed for high earners to maximize tax deductions and is locked until age 62. In contrast, a Private Pension Germany plan offers more flexibility and liquidity regarding withdrawals, making it a better choice if you need access to capital before retirement.

What is the first step for effective Retirement Planning Germany?

The best place to start your Retirement Planning Germany journey is by auditing your current income and securing your earning ability with disability insurance (BU). Once your income protection is in place, you can move on to building a diversified Self Employed Pension in Germany portfolio.

Can a Freelancer Pension Germany plan help reduce my annual tax burden?

Absolutely. Many financial products, especially the Rürup Pension Germany, are highly tax-efficient. By investing in a well-structured Freelancer Pension Germany plan, you can deduct significant contributions from your taxable income, lowering your overall tax liability while saving for your future.

What is the most flexible option for a Self-Employed Pension in Germany?

If flexibility is your main priority, a private pension contract often allows for more adjustments, such as pausing or increasing contributions, compared to rigid state-subsidized models. It is highly recommended to compare different products to see which Retirement Planning Germany strategy best aligns with the fluctuating income typical of a Freelancer Pension Germany holder.

What happens to my accumulated retirement savings if I decide to leave the country?

It depends on your contract structure. Most private pension plans remain valid regardless of where you live, meaning your capital continues to grow. However, your tax residency will change, which may impact how your future payouts are taxed. Always review the “portability” clause of your specific policy before relocating to ensure your long-term wealth strategy is secure.

Should I invest directly in ETFs or choose an insurance-wrapped retirement plan?

This is a key decision for any long-term investor. Direct ETF investing offers maximum liquidity and the lowest cost structure. In contrast, an insurance-based wrapper can provide the Halbeinkünfteverfahren tax advantage for long-term holders. Choosing between them depends on whether you prioritize immediate access to your funds or long-term tax efficiency.

Does the statutory pension system offer better value than a personal retirement plan?

The state-run system functions primarily as a social safety net and often yields lower long-term returns compared to diversified capital market investments. Most high-earning professionals prefer a personal plan because it offers higher potential growth and greater autonomy over how their money is invested.

What is the fundamental difference between “Brutto” and “Netto” in pension contracts?

In the industry, “Brutto” contracts often include hidden sales commissions that are deducted from your initial capital. “Netto” (commission-free) contracts remove these distribution fees. Choosing a Netto product ensures that a significantly higher percentage of your monthly contribution goes directly into your investment portfolio rather than paying for sales overhead.

Do I really need a tax advisor (Steuerberater) for my retirement strategy?

While not strictly mandatory, professional guidance is highly recommended. A tax advisor ensures that your contributions into tax-deductible financial vehicles are correctly reported in your annual Steuererklärung. This professional oversight is often what makes the difference in securing the maximum possible tax refund each year.

Ready to Plan Your Retirement with Confidence?

Retirement planning isn’t about finding a single “perfect” pension product—it’s about building a strategy that aligns with your goals, career and future lifestyle.

If you’re an expat living in Germany and you’re unsure whether you’re making the right retirement decisions, a personalised financial review can help you understand your available options and identify potential gaps in your current plan.

During your free initial consultation, we’ll discuss:

✅ Your current retirement position

✅ Your pension options as a self-employed professional

✅ Tax-efficient retirement planning opportunities

✅ Long-term investment strategies

✅ Practical next steps based on your personal goals

Whether you’re just starting your business or already earning a high income, having a structured retirement strategy today can make a significant difference in your financial future.

👉 Book your free consultation today and start building a retirement strategy designed around your life, not assumptions.

About the Author

Sara Rahimi is a licensed Financial Consultant in Germany, specialising in retirement planning, investment strategies and wealth building for expats.

She works with international professionals, freelancers and business owners across Germany, helping them understand the German financial system and build long-term financial security through personalised planning.

Her mission is to make complex financial topics easier to understand by providing practical, transparent and educational guidance tailored to the unique challenges expats face while living and working in Germany.

Disclaimer

The information provided in this article is intended for general educational and informational purposes only and should not be considered financial, tax or legal advice.

Retirement planning in Germany depends on individual circumstances, including your profession, income, residency status, tax situation and long-term objectives. Laws, regulations and tax rules may also change over time.

Before making financial decisions, you should consider obtaining personalised advice based on your specific circumstances.

While every effort has been made to ensure the accuracy of the information at the time of publication, no guarantee is given regarding its completeness or continued accuracy. Readers remain responsible for verifying any information before acting upon it.

Leave a Comment

Have a question or experience to share? Drop a comment below.

Leave a Comment